📢 Attention All Researchers and Consultants!

Update: “Criteria for Calculating Reference Prices for Consulting Services”

New Edition from the Public Debt Management Office, Ministry of Finance (March 2026) 📢

To ensure your project proposals are accurate and processed efficiently, TU-RAC has summarized the 4 key points you need to know:

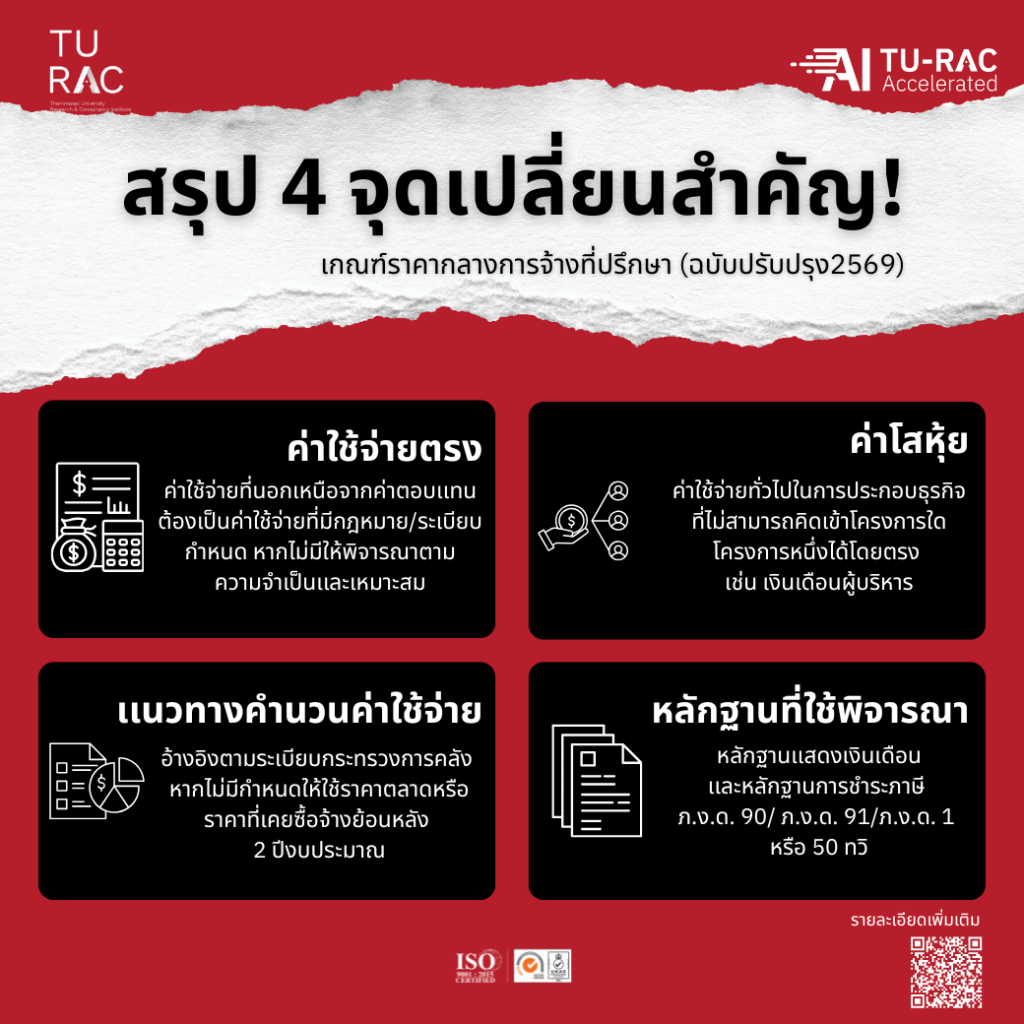

1️⃣ Direct Costs: The definition has been updated to cover other necessary expenses beyond personnel fees. (These must be based on official regulations or market prices; if neither is available, they will be considered based on necessity and appropriateness.)

2️⃣ Overhead: Now clearly defined as general business operating expenses that cannot be specifically allocated as a direct cost to a particular project.

3️⃣ Calculation Guidelines for Direct Costs: Calculations must refer to Ministry of Finance regulations or be supported by market price surveys/actual historical hiring costs.

4️⃣ Supporting Documentation for Consultant Hiring: To calculate the Basic Salary, a salary certification letter and tax evidence (such as P.N.D. 90/91/1 or 50 Tawi) must be provided to ensure compliance with the new criteria.

💡 Advice: Researchers should study these updates and prepare all documentation according to the 2026 criteria to minimize project revisions.

📂 Download further details at: https://tu-rac.com//file-store/scan_file/scanOut_42824_20260320132241.pdf